Inheritance in Web3: Passing Crypto to the Next Generation

Degens aren’t exactly known for being careful with their capital, but once the crypto riches begin to stack up, many will want to make sure the wealth can support their families and loved ones after they’re gone.

Whether you’re making plans for what happens after you pass away - or become incapacitated for whatever reason - considering what could happen to your crypto is an important part of the process.

For those who embrace the ethos of “not your keys; not your coins,” that means coming up with a plan to “pass your keys; pass your coins.”

The question is, how do you do that?

The Importance of Planning

Famous Bitcoin Losses

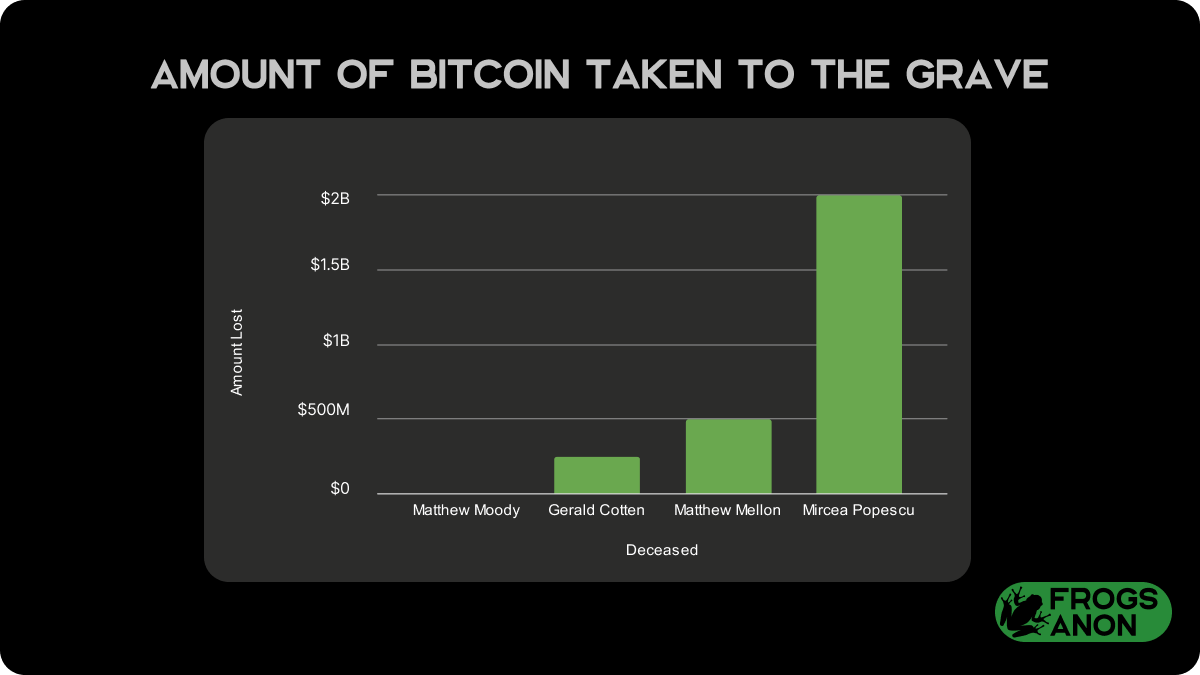

The problem of crypto inheritance isn’t exactly new. People die with large amounts of crypto all the time, with several events previously making headlines. Consider:

Banking Heir Matthew Mellon’s loss of $500 million in XRP in 2018.

Quadriga CEO Gerald Cotten, who left his Canada-based exchange with $250 million in debt after his death in 2018.

Mircea Popescu, known for having one of the largest bags in Bitcoin, drowned off the coast of Costa Rica in the summer of 2021 with an estimated $2 Billion worth of Bitcoin.

Early Bitcoin miner Matthew Moody, who passed in 2013 with around $50,000 worth of Bitcoin (at today’s prices) his father has been unable to recover.

Unfortunately, the intricacies of managing your own private keys become even more difficult when you start thinking about how to transfer them to another person in a safe manner.

The Difficulty of Key Management

The hard part of crypto inheritance is creating a safe process to transfer control of your digital assets to the right person.

No matter what method you use, you’ll need to make sure the recipient understands the basics: how to use a digital wallet, how to use a digital exchange, and basic safety tips to ensure the recipient avoids common mistakes people make when using crypto.

There are two ways you can go about transferring your assets to another person; each with its own pros and cons.

1. Transfer the private key

The first, simplest method of transferring assets involves storing a copy of the private key somewhere and providing a way for the heir to retrieve it. The primary challenge with this method has to do with where the owner decides to store their private key.

For some, using a safety deposit box that heirs can only access after obtaining a death certificate or some other form of legal permission could be the safest method to use. For others, simply storing the private key in a private location - in a safe, perhaps - is the way to go.

The ideal place to store a private key minimizes the risk that it could be seized by a third party (like a bank or your lawyer, if you choose to get them involved) as well as the risk that an heir could, willfully or unwillingly, take the private key before the owner wants them to have it.

Pros

- This method is easier to set up than the other method because it doesn’t involve deploying a smart contract.

Cons

- Storing a private key always entails the risk that something could happen to the private key itself or that someone else could find the private key before the intended recipient.

2. Transfer the Assets

The second method involves setting up a smart contract to automatically transfer some or all of your assets to digital wallets controlled by the intended heirs.

This typically involves setting up a “dead man’s switch,” which requires the user to check in before a programmed timer expires. If the timer goes off, the smart contract can be configured to automatically transfer some or all of the assets held in the wallet or transfer control of the wallet to their intended heirs.

Assets can be transferred to different wallets for different heirs or moved to a single wallet for a single heir. Other features could be added to provide extra features, like requiring one or more “executors” to sign transactions before the assets get transferred.

Pros

- Because this method takes place on-chain, it inherits the censorship resistance and security of the underlying blockchain.

Cons

-

This method is more difficult to set up because it involves deploying a smart contract.

-

There’s also the risk the recipient’s private key could be compromised, with or without their knowledge, before they can claim their inheritance.

Examples

Metaverse Solutions...

While these are the options available today, the potential development of technologies like Soulbound tokens and decentralized identity could unlock new avenues for verifying whether or not an individual has died or become incapacitated.

Soulbound tokens or other forms of decentralized identity could be connected to existing services that detect when an individual has passed away, allowing individuals to forget about the dead man’s switch and automate the transfer of their assets to a different wallet.

While the technology needed to create and manage decentralized identities already exists, we don’t yet have a robust ecosystem for creating identities that anyone will trust.

Your ID may be useful to you because it has your name and picture on it, but the only reason it matters to anyone else is that it carries the security features implemented by the licensing office.

Perhaps in the future, coroners can join the fun in the metaverse, and oracles will be able to draw data from an API at the Office of Vital Records. Then the execution of a smart contract could be conditional on the filing of a legal death certificate, and inheritance will be automated on-chain.

Today, however, this is simply a distant fantasy. Accessing death records in even a single country can be extremely difficult due to the regulations on this type of data. For now, being your own bank also means being your own executor.

Not Your intent, Not Their Coins

Regardless of which method you choose to help your loved ones access your assets, it’s critical to consider the legal implications of your process.

If a jealous family member discovers you gave crypto to an heir without a will or any formal documentation expressing your wishes, for example, they could potentially take legal actions that make things difficult for your loved one.

Using a smart contract to automate the transfer of your assets involves making a public transaction that anyone will be able to see. In most cases, this shouldn’t be an issue, but it could cause problems if someone decides to dispute the way the assets have been distributed.

Even if it’s “not their keys; not their coins,” it’s worth considering whether or not your actions could subject your loved ones to legal problems, especially at a time when they could already be dealing with a difficult situation.

Plan Before it's Too Late!

Making plans and talking about what you want to happen after you’ve passed away may be difficult, but anyone who’s had the responsibility of handling a loved one’s assets knows what a difference it can make.

Having a good plan can significantly reduce the time it takes loved ones to access the money by weeks, months, or even years. If it minimizes the hardship they’ll face when handling such a difficult situation, why not take the time to get a plan together?

Unless you truly don’t care what happens to your money after you die, make a plan to ensure your assets can be transferred, and talk to your loved ones about your wishes and what they need to know to access and use your assets.

To those that matter most, it could make a world of difference.

Published on Jan 04 2023

Written By:

Seth Goldfarb

@GoldenChaosGod